ETF Killer

The most tax-efficient index

Disclaimer / Disclosure My family and I are long each of the Frec direct indexes listed below.

Frec lets you get started in just two minutes with as little as $20k. It employs direct indexing, a common strategy among family offices. It is the most tax-efficient way to invest in diversified equities. In the past this took a far larger scale because it was implemented by hand. But with AI, Frec can efficiently and automatically harvest tax losses within your direct index at almost any scale. Over a decade,

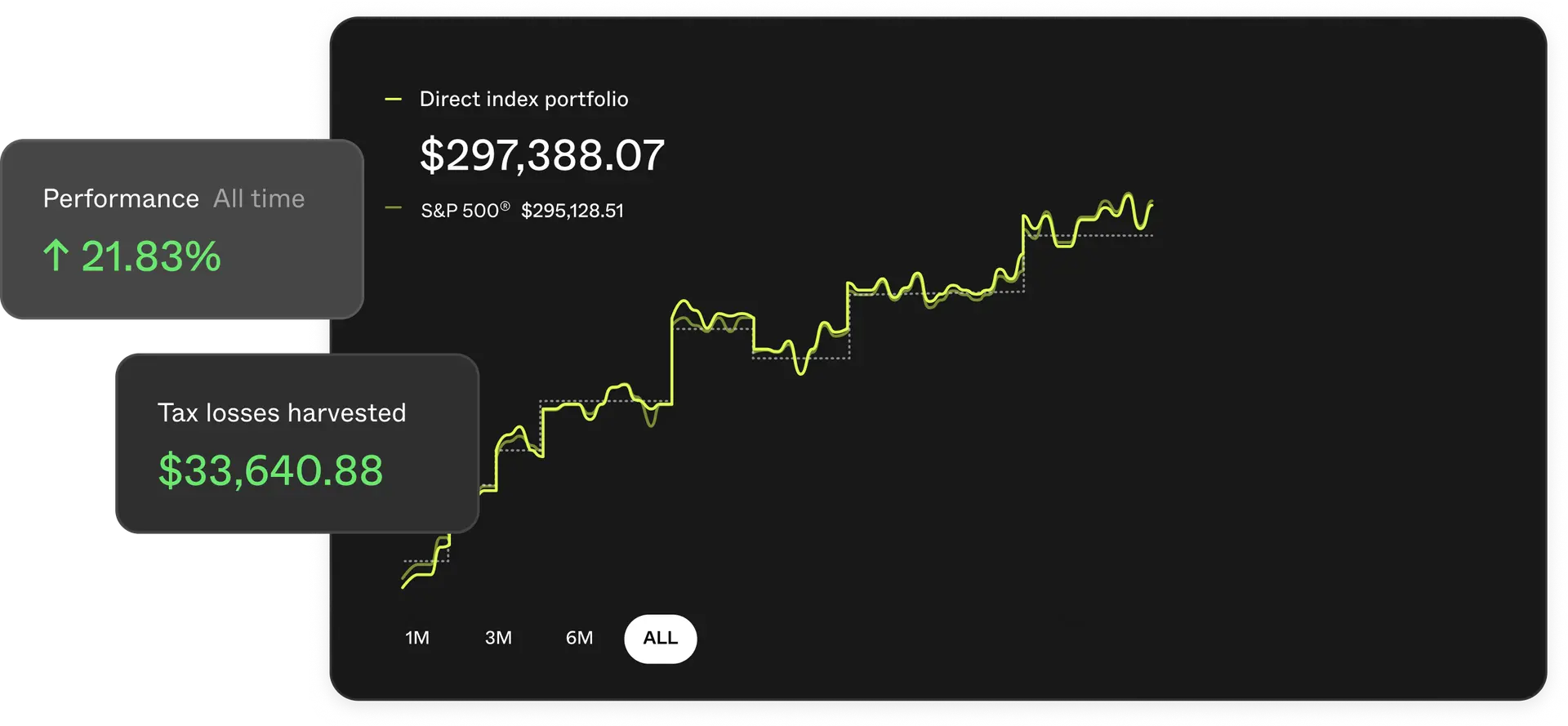

Their Treasury fund earns >4%, above the 4% currently offered on Robinhood Gold (HOOD). I funded that cash account as well as the S&P Developed Markets ADR index and the CRSP US Large Cap Value index. While both are up over the past three years, the first harvested >22% tax losses while the second harvested >18%, significantly boosting after tax wealth. If you pursue special situations and event driven opportunities, you might get short-term capital gains which these direct indexes can offset. My next allocation will be to the S&P Emerging ADR index but cutting the TSM and BABA allocations in half in order to dampen excessive Taiwan invasion risk. Then I’m setting aside a few hundred k in the Treasury fund to allocate to their new long-short fund when it launches next month.

So far setup has been utterly seamless. The site is well designed and undistracting. This is not an account for entertainment value. It is the ‘end’ for my money, the place where I put capital that I never intend to touch again. If I ever need liquidity, I’ll just use the portfolio line of credit. I leveraged my value index 25% with their line of credit. It charges ~5%, automatically billing my bank account.

Looking at my life expectancy relative to my children’s ages, the bulk of their inheritance could come when it’s least needed at the peak of their earning years and past the bulk of their family expenses. The most likely year for their inheritance is in the last 2050s or early 2060s when my kids will be well past middle age. I want to start far sooner. I have different structures for minors but when they are adults my plan is to deposit $20k each in their direct indexes each year then match any direct deposits that they commit to up to $1,500 per month, staying within gift tax exemptions and encouraging them to save. I will strongly encourage them to never withdraw any of this money (which will also be a precondition of subsequent gifts).

Caveat

I hope to outperform this tax-efficient passive allocation over the long-term with my active ideas, but this is the standard: a tax-efficient ~10% annualized return for multiple decades.

Conclusion

I expect to save millions of dollars from getting squandered on excessive taxes by direct indexing instead of buying ETFs; you might want to too.

TL; DR

Get >4% on your cash, lower taxes than ETFs, and a $250 sign up bonus.

Thanks Chris. Does it feel like long-term, you'd have to keep adding capital to the account to keep harvesting gains? Particularly on a mean reverting strategy like value.