Amping Up

Going from 180% to 400% gross

Disclaimer / Disclosure long Frec

Direct Indexing

140/40 long short direct indexing is available here. Direct indexing allows for improved tax efficiency through ongoing, systematic loss harvesting. My current 140/40 long short portfolio takes a 140% long position and a 40% short position. Proceeds from the 40% short sale fund the additional 40% long exposure, keeping the net market exposure close to 100% and consistent with the benchmark index.

The long short design enhances tax loss harvesting in a variety of market environments. When markets decline, the long side of the portfolio tends to accumulate losses that can be harvested. In rising markets, shorts can generate realized losses as prices move against them—providing opportunities to offset capital gains. This dual-sided mechanism enhances the consistency and volume of tax loss harvesting.

My own realized results with Frec are a 27% pre-tax IRR with a 22% tax loss harvesting IRR over the same period. Frec has also run simulations across various market environments that are consistent with my experience. Long short offers greater net excess returns than long-only because of more tax alpha:

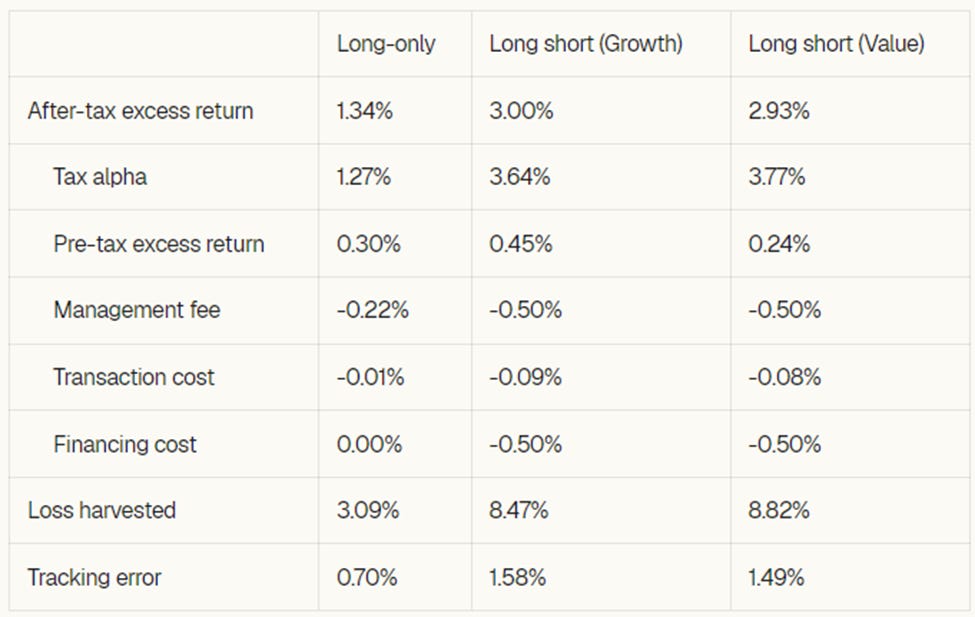

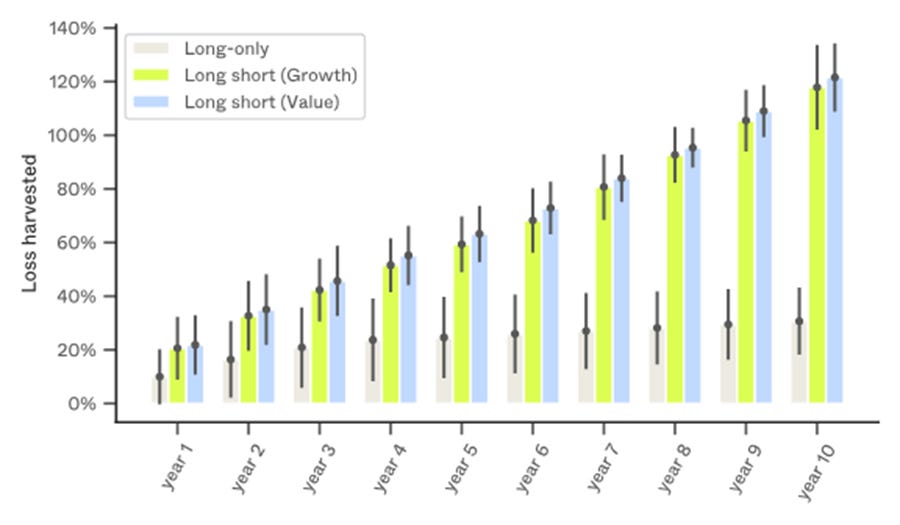

According to Frec’s simulation,

On an after-tax basis, both the growth-tilted and value-tilted long–short strategies deliver superior performance relative to a long-only direct indexing approach, with annualized after-tax excess returns of 3.00% and 2.93%, respectively, compared with 1.34% for the long-only portfolio. This outperformance is driven largely by tax efficiency. The long short strategies realize substantially more harvested losses (8.47% for growth and 8.82% for value, versus 3.09% for long-only), which translate into tax alpha of 3.64% and 3.77%, respectively. Despite its higher transaction costs (0.09% for growth and 0.08% for value, versus effectively 0.01% for long-only) and a financing cost of 0.50% (which the long-only strategy does not incur), the long short strategies’ enhanced tax benefits more than compensate for these implementation frictions.

Higher leverage

Here’s what happens when more leverage is applied:

Frec’s simulation shows that:

Increasing leverage scales the strategy’s outcomes. The 250/150 strategy, for example, generates a significantly higher pre-tax excess return (1.10%) and a much larger volume of realized losses (19.16%), leading to the highest after-tax excess return net of fees (6.63%). This outperformance, however, is accompanied by a proportional increase in costs and a materially higher tracking error (4.13%), underscoring the direct relationship between the magnitude of the leverage, implementation costs, and the portfolio’s deviation from the benchmark.

Caveat

> leverage = > tracking error.

Conclusion

The long short strategy offers greater tax efficiency than long-only. Across all simulation periods, it generated higher levels of harvested losses and post-tax returns even after higher fees. This tax alpha is especially valuable for investors in high marginal tax brackets seeking to reduce taxes.

TL; DR

This is my favorite way to passively invest for the long-term. More leveraged l/s > less leveraged l/s > l only for tax alpha. 140/40 long short direct indexing is available here. I own it but will switch to 250/150 once that becomes available shortly.

Lol, i thought we were getting back into AMPY for 2026 when I saw the headline. Releived at topic!